"The New Financial Order—Until It Collapsed" by Roger Lowenstein (NYRB)

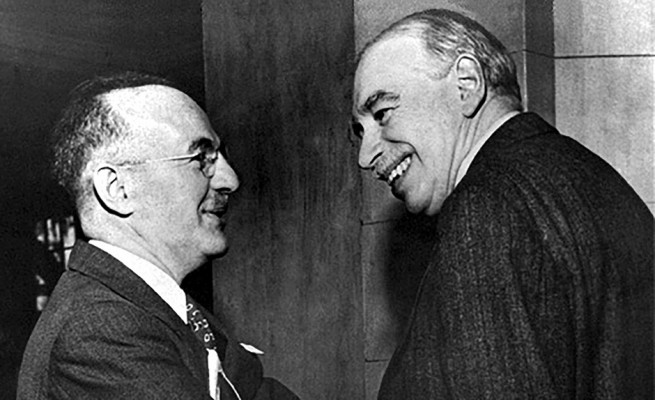

[IMF CollectionUS Assistant Treasury Secretary Harry Dexter White and the British economist John Maynard Keynes at the inaugural meeting of the International Monetary Fund and World Bank’s board of governors, Savannah, Georgia, March 1946]

he Summit: Bretton Woods, 1944: J.M. Keynes and the Reshaping of the Global Economy by Ed Conway Pegasus, 453 pp., $28.95

by Ed Conway Pegasus, 453 pp., $28.95

The world’s monetary system moves from tumult to tumult. Europe’s economy is stagnant and menaced with deflation. Greece has flirted both with leaving the euro and with default. America’s economy has fallen into a discouraging pattern of hopeful growth spurts followed by dispiriting slowdowns. Such turmoil has played havoc with world currencies. Late last year, the value of the euro crashed. Earlier this year, the cautious Swiss stunned traders by freeing their currency, permitting it to soar against the euro and raising—sharply—the price of its chocolates and ski chalets for people from Lisbon to Rome. Such volatility has lately been increasing. If, as the Harvard political scientist Jeffry Frieden has asserted, “the exchange rate is the single most important price in any economy, for it affects all other prices,” then global economies have rarely looked so unstable.(1)

Lately, the instability has spread to Asia. Since 2012, the Japanese yen has lost nearly a third of its value. This has enhanced the competitiveness of Japanese products, putting pressure on its Asian neighbors. China’s economy—in recent years the biggest contributor to the world’s growth—is rapidly decelerating. In August, China stunned markets by devaluing its currency. As for the US, the dollar has risen sharply against the euro and other currencies, but this rise has put America’s fragile recovery in jeopardy, by rendering its manufactured products less affordable overseas. And it has spelled bankruptcy for some of the foreign firms that borrowed in dollars (now too expensive for them to repay). A certain amount of gyration among currencies is normal, of course; that is what currencies do. But the instability has been alarming to traders, businesses, and statesmen.

Since the financial crisis, individual banks have been subject to a welter of new laws and regulations, but not so the international monetary system in which they operate. This system serves as a conducting rod for transmitting local disturbances around the globe. Even this metaphor presumes too much, for the international monetary “system” is, in fact, not a system at all. Its various pieces are simply too disjointed. America and most countries in the West permit capital to freely cross their borders. But China, the most important emerging power, tightly controls the movement of capital.

If, say, Coca-Cola wants to build a factory in China, it must apply to the government to exchange dollars for local renminbi. Many other emerging countries maintain weaker, or periodic, capital controls. Some allow their currencies to float; others “peg” them to the euro or the dollar. Switzerland maintained such a peg—until, in January, it didn’t. The dollar is the linchpin—the usual standard for other currencies and for international trade. However, no agreement or formal convention assures the dollar of its pivotal role. Most nations keep most of their reserves—the assets they hold to make international payments, such as on their debts and trade—in dollars but they could, if they wanted, abandon the dollar tomorrow.

Persistent financial turmoil has led to demands for reform or reinvention of this ad hoc system from advocates such as Joseph Stiglitz, the Nobel laureate economist, George Soros, the investor, and Zhou Xiaochuan, the long-serving governor of the People’s Bank of China (the central bank). Not surprisingly, it has also reawakened interest in the one period when exchange rates, rather than being left to the caprice of events, were governed by international agreement. Roughly from the end of World War II until the early 1970s, the world’s currencies were locked at fixed rates of exchange to the dollar, which served as the reserve currency, interchangeable with all others. This was the so-called Bretton Woods system, named for the mountainous retreat in New Hampshire where, in the summer of 1944, forty-four Allied nations convened to hammer out a monetary agreement.

Bretton Woods was a response to a problem that bedeviled international markets in the 1930s and bedevils them today. To put the problem simply, some countries are likely to produce more efficiently and compete more effectively, and thus to accumulate a trade surplus; others, perforce, will run deficits. Importing nations can paper over these deficits by borrowing, but in a world in which capital is free to move from country to country, speculators may sooner or later provoke a run on their currencies. Eventually, the pressure for adjustment becomes intense.

One solution is for deficit nations to raise interest rates, which will lure capital home. But high interest rates, while they may be a remedy for the currency imbalance, can be painful to the domestic economy and cause recessions. Alternatively, deficit countries can devalue their currencies, which will discourage imports and encourage exports. But devaluations destabilize entire sectors of the economy that depend (or whose raw materials depend) on trade. Moreover, when one country devalues, others often follow. To avoid this trap, countries have experimented with various forms of controls.

Bretton Woods was an attempt at collective controls. For the quarter-century that it lasted, it was also a marked success. Under Bretton Woods, the world’s economic output rose at an annual rate of 2.8 percent, well above the 1.8 percent registered from the early 1970s until the 2008 financial crisis. And while the epoch of the gold standard during the late nineteenth and early twentieth centuries is reverently invoked by free-market purists, growth under the managed system of Bretton Woods was twice as swift.(2)

What’s more, under Bretton Woods, capital imbalances among nations were relatively muted and banking crises were rare, as were defaults by countries on “sovereign debts”—the money borrowed directly by governments. During the Bretton Woods period, inflation was high, but standards of living rose around the globe. Banking represented a far smaller share of economic output than in the freewheeling financial climate that has prevailed lately, and inequality was less pronounced. If Bretton Woods cannot claim credit for all of these conditions, it was part of an architecture of financial regulation that, since the 1970s, has been relentlessly dismantled.

Why did Bretton Woods succeed, at least for a time, and does it suggest a prescription for would-be reformers today? The Bretton Woods agreement was cobbled together in July 1944, barely a month after the Allied landings in Normandy, when seven hundred delegates crammed into an aging and hurriedly refurbished hotel. The delegates, many of whom did not share a common language, worked unceasingly for three weeks and—while drinking copious quantities of alcohol—ratified a plan to manage the currencies of the world. “No one had ever successfully modified the international monetary system,” Ed Conway relates in his sweeping account, The Summit: Bretton Woods, 1944. “Instead,” in prior epochs,

it had evolved incrementally—from the early days of mercantilism to the British Empire–dominated gold standard which collapsed in 1914, through to the flimsy system of currencies and rules erected after the Great Depression in the 1930s. All previous efforts to achieve what the delegates were attempting had failed, without exception.

The delegates were motivated to reach agreement, as Conway emphasizes to good effect, because they were all aware of prior failures, notably the Versailles conference after World War I. They were laboring not just to create a new financial order but to prevent another depression and another world war. This was especially true of the conference’s stars, England’s celebrated economist John Maynard Keynes and the American assistant treasury secretary, Harry Dexter White.

Conway uses Versailles as a historical precedent, quoting Britain’s David Lloyd George, who ominously predicted when the treaty was signed in 1919, “We shall have to do the whole thing over again in twenty five years.” Conway adds: “He had predicted the date of Bretton Woods almost to the day.” It is a perfect introduction to the various interwar efforts to patch up the monetary system, none successful, that lent such purpose to Bretton Woods.

Many previous books have chronicled the conference, including a very good one in 2013, Benn Steil’s The Battle of Bretton Woods.(3) Steil’s account focused more tightly on the conference as a battle between two luminaries who squared off at diametrically different points in their respective countries’ fortunes. Harry White asserted American interests at the moment the US emerged as a dominant superpower; Keynes, serving as an unpaid adviser, was trying to stave off national bankruptcy.

Ed Conway has made use of a wide range of archives, including recently available Soviet files; he emphasizes the conference’s international, as distinct from its bilateral, character. But he, too, centers the plot on the large personalities from America and Britain. His description of Keynes is captivating even if familiar. After participating in—and then publicly denouncing—the Versailles Treaty, Keynes became a public intellectual sought out by statesmen and a best-selling writer on economics. Tall and thick-lipped and dizzyingly self-confident, he had been, earlier, an almost voluptuous figure in the Bloomsbury set. He was actively homosexual but married a Russian émigré ballerina, Lydia Lopokova. Conway provides some details not often found in monetary histories, quoting a letter in which the devoted Lydia professes to Keynes, “I lick you tenderly.”

If White, nine years younger than Keynes, was hardly so bohemian, his rise was more improbable. The son of a Boston hardware store owner, raised with progressive sympathies, he took an interest in politics and chose to study economics, including the socialist economics of Russia. At age forty-two he left a dim career in academia for a job at the Treasury, where he quickly became the right-hand man of Roosevelt’s treasury secretary, Henry Morgenthau Jr. Round-faced and a foot shorter than Keynes, he was brilliant and also unpleasant. Keynes found White to be “over-bearing…aesthetically oppressive in mind and manner.” Nonetheless, he recognized that White was an innovative thinker who could distill economics with clarity. He also cited his “high integrity.”

Each man wanted to do away with the wild currency swings that destabilized Europe’s democracies and poisoned international relations in the 1930s. Keynes was also keen on eliminating the gold standard. Before World War I, and in some nations after it, countries pledged to redeem their currencies in gold; nations that ran short were often forced to curtail employment and growth. In the interwar period in Britain, allegiance to the gold standard provoked a severe recession. Although Keynes objected on philosophical grounds to hitching national economies to the vagaries of gold supplies, his crusade was also stiffened by national interest. The war with Nazi Germany rapidly emptied Britain of what little gold it had. As early as 1940, Conway relates, the British ambassador cheerfully told reporters in New York, “Well boys, Britain’s broke; it’s your money we want.”

Early in the war, Keynes proposed an international bank, which he termed a Clearing Union, to regulate global finance in the postwar world. This bank would issue a new currency (dubbed “bancor”) that would gradually replace gold in international finance—a shrewd proposal, since most of the world’s gold by then was in America. Nations that ran short of currency could borrow from the Clearing Union; just as importantly, the Clearing Union would penalize countries that had a trade surplus and accumulated too much currency. The genius of this scheme was its symmetry. During the 1930s, Keynes observed, the process of adjustment was “compulsory for the debtor and voluntary for the creditor.” In other words, importing nations, as they ran short of foreign exchange, had no choice but to curb their imports or to devalue, while exporting nations could run up surpluses forever. Britain in particular suffered, since its industry was uncompetitive. It needed—and during the war Keynes earnestly sought—protection from cheaper foreign goods.

Gamma-Keystone/Getty ImagesA demonstration against the Bretton Woods agreements, London, December 1945

Gamma-Keystone/Getty ImagesA demonstration against the Bretton Woods agreements, London, December 1945

America, though, refused to offer such protection. As the world’s biggest producer it had no interest in restraining exports. This is an irony—more fully teased out by Steil—given that, today, America runs a persistent trade deficit, and habitually complains that exporters such as China tilt the scales by depressing their currencies and so achieve higher sales abroad. Keynes’s plan would have solved all that. But Keynes and Britain were in no position to bargain.

White had also worked up a plan, which he finished several months after Pearl Harbor. Although the two plans agreed on much, including fixed exchange rates, White’s prescription, Conway notes, would “ensure that the outgoing superpower [i.e., the UK] would be shuffled even further from centre stage.” After a period of Anglo-American negotiations, Morgenthau and White issued general invitations to the Allied nations to attend a conference on the international economy. Conway vividly conveys the chaos at Bretton Woods, which Keynes likened to a “monkeyhouse”—journalists snoozing on chairs, Russians drinking with everyone and negotiating with no one.

There was a secret drama shadowing White, who in the late 1930s and apparently in the early 1940s regularly provided confidential information to Soviet couriers, including Whittaker Chambers, who relayed his information to Moscow. Decades later, a Senate commission would conclude that White’s complicity in espionage “seems settled.” Steil generally endorses this conclusion; Conway is more equivocal. He notes that the Soviets were then America’s ally, and finds no evidence that White was a Communist. He simply believed, Conway argues, that after the war Soviet–American cooperation would be vital to peace, and desperately wanted the Russians to be a part of the new order. Conway’s view may be generous, but White’s ties to Moscow are tangential to his work at Bretton Woods. In both Steil’s and Conway’s judgment, White emphatically pursued American interests there. (He did obtain generous terms for the Soviets, but as Stalin ultimately refused to join the system, they were never carried out.)

The final document was faithful to the American agenda. It provided for an “International Monetary Fund,” headquartered in Washington, D.C., which would offer emergency loans to member nations. The IMF would also be empowered to impose harsh austerity measures on borrowers, demanding, for example, that they reduce their deficits. Keynes had hoped for a more benign institution, one that dispensed everyday loans for routine trade, but it was not to be. The agreement also created the World Bank to assist in development. Keynes envisaged that the bank would be pivotal to European recovery, but—again—America had other ideas. In the immediate postwar period the bank was reduced to irrelevance by the Marshall Plan.

While White had no use for a contrived currency such as bancor, he recognized that the gold standard had imposed harmful rigidities on the world economy. His solution was to banish gold from sight but not quite from mind. Each currency would be convertible into dollars; additionally, foreign central banks could, if they chose, demand that the US convert their dollars into gold. Thus, Bretton Woods authorized dollars as the universal medium—but only so long as other nations would accept them. In the climate of 1944, when dollars were scarce and hotly coveted, this hardly seemed a serious risk.

The other philosophical chasm between White and Keynes concerned the degree to which currencies other than the dollar would be freely convertible. Keynes, previously an avid currency speculator himself, was wary of letting traders move money around the globe. He feared that speculation would lead to currency upheavals and that Britain in particular would be vulnerable. White, once again, prevailed. Keynes, who died in 1946, lived long enough to predict, correctly, that convertibility would lead to a run on the pound—“a financial Dunkirk.”

White was not permitted to enjoy the new order any more than Keynes. He had aspirations of managing the IMF, but by 1947 he was under FBI surveillance. In 1948, he was grilled by a congressional committee and firmly denied Communist allegiance. He then suffered a heart attack and died.

A decade of monetary stability followed Bretton Woods. A major reason was that, as Conway notes, the transition in Europe toward free movement of capital was slower than anticipated. Conway might have made more of this. Robert Mundell, the Canadian economist and Nobel laureate, has postulated that of three possible choices—a domestic monetary policy, fixed exchange rates, and the free movement of capital—countries can have two, but not all three. During the first dozen years of Bretton Woods, the first two obtained but not the third. “Only in 1958,” Conway writes, “did European countries finally restore convertibility.” Restrictions were then removed on currency exchanges for goods and services (though not for currency speculation). In the 1960s, the capital trickle became a powerful stream.

“As capital became more mobile, it became more difficult to maintain exchange rate pegs,” Eric Helleiner, a Bretton Woods scholar at the University of Waterloo, Ontario, told me. In the late 1960s, speculative pressures forced revaluations. Also, dollars began to pile up in foreign central banks. Valéry Giscard d’Estaing, the French finance minister (and later president), accused America of enjoying an “exorbitant privilege.” He meant that only the United States could churn out an endless supply of the universally acceptable currency (dollars), while other countries had to actually produce and export goods to obtain them. Ultimately, various European nations began to exchange dollars for gold. As America’s gold reserves began to dwindle, the system wobbled. In 1971, President Nixon was forced to end the pledge to convert dollars into gold. Quickly, the entire system of fixed rates collapsed. The problem was that Bretton Woods had pretended to banish gold but hadn’t actually done so. Steil concluded that Bretton Woods died “of its own contradictions.”

Over the next decade or so, restrictions on capital in the developed world were swept away. Similar reforms were pushed in the developing world by the IMF, which took the inflexible view that countries gain more than they lose by permitting capital to flow across borders. Since many emerging countries were dependent on the IMF for loans, the IMF was able to enforce significant liberalizations.

But remarkably little changed for the dollar. Today it remains the principal reserve currency. Giscard d’Estaing, now eighty-nine, must be astonished that Americans still enjoy the “privilege” of a world with a seemingly endless appetite for its money. Though America runs a trade deficit year after year, foreign central banks are quite content to loan their surplus money to the US—which borrows from them at very low rates of interest. At present, emerging countries, led by China, hold a staggering $7 trillion in US Treasury bonds and other forms of dollar-denominated debt. Predictions that the dollar will crash, accompanied by a foreign exodus from US Treasury bonds, have become a staple of economic forecasters. Numerous potential substitutes have been proposed—the yen, the euro, the renminbi. As China’s share of the world economy grows, the renminbi is said to be the most likely candidate to replace the dollar, although it is still far from fulfilling the requirements of a reserve currency. It is not convertible, and the Chinese government is not sufficiently transparent. Another possibility, suggested by the economist Barry Eichengreen, is that the dollar may be partially dislodged by a group of currencies.(4)

But since the recent financial crises, the dollar’s position as a safe haven has only strengthened. “The great paradox,” the late Ronald McKinnon pronounced at a Bretton Woods anniversary gathering last year, is that although the dollar is distrusted because of the US trade deficit, governments and private traders “still consider it the best option.”

The speculation about which currency might (eventually) replace the dollar seems in any case beside the point. What ruffles markets and world economies now is not the centrality of the dollar but the absence of coherence. In recent months, central banks in Denmark, Singapore, Turkey, Russia, the eurozone, and elsewhere have launched programs to create inflation in their local currencies. They do so by issuing more currency, potentially leading to higher prices. Although the banks are motivated by domestic concerns (they are trying to stimulate their local economies), their actions are suggestive of the currency wars that disrupted trade during the Great Depression. Early this year Mike Newton, a former trader, wrote in a frantic-sounding Wall Street Journal Op-Ed, “The situation demands policy coordination.” This was the staple cry of the 1930s.

Conway does not think world leaders have the will to stage a second Bretton Woods. It is not, however, a question of will but of priorities. A Bretton Woods II would cure volatility, but it would require braking the flow of speculative capital. For many smaller or emerging countries there has, in fact, been some small movement in that direction. For instance, Brazil has imposed a tax on foreign investments in its stock market. “Interest in the use of capital controls has grown in the wake of the Great Recession,” according to Michael W. Klein, an economist at Tufts University.(5 ) Even the IMF has abandoned its orthodox opposition to capital controls in emerging nations. The arguments for deliberalizing capital boil down to two: first, countries that do not accept speculative inflows are less vulnerable to panicky withdrawals, such as those that pummeled formerly high-growth Asian states in 1997; and second, China’s remarkable growth was achieved without liberalizing its controls over capital, which have minimized the ability of speculators to place bets on China’s currency.

Nonetheless, most controls (China’s excepted) have either been transitory or ineffective. China, which permits trading of its currency only within a narrow band of values, is itself coming under speculative pressures that could one day force it to adopt a more free-market approach. And there is little support for controls in the developed world. Two generations of bankers, hedge fund traders, and world leaders have been conditioned to believe that capital should be permitted go where it wants, whatever the upset it may cause to trade, and at whatever risk of speculative bubbles. Western economies once combined private enterprise with restricted capital markets; those days are gone. As Jeffry Frieden told me, “The genie cannot be put back in the bottle.”

Conway sounds almost mournful, even though he calls the 1944 agreement flawed. “In this messy world,” he concludes, “Bretton Woods has come to represent something hopeful, something closer to perfection.” He does not say what that something is—presumably, the lost ideal of equilibrium. Bretton Woods reflected a decision—after the turbulence of depression and war—in favor of stability. Today’s pundits may lament the volatility of international capital, but modern leaders, and by extension their electorates, have preferred the mixed benefits of unchecked capital mobility. We will continue to have turmoil over trade and unstable currencies, because that is what most nations want.

- 1 - Currency Politics: The Political Economy of Exchange Rate Policy (Princeton University Press, 2014), p. 1.

- 2 - See Ed Conway, The Summit: The Biggest Battle of the Second World War—Fought Behind Closed Doors (Little, Brown, 2014), p. 388.

- 3 - Council on Foreign Relations/Princeton University Press, 2013; reviewed in these pages by Robert Skidelsky, January 9, 2014.

- 4 - See Exorbitant Privilege: The Rise and Fall of the Dollar and the Future of the International Monetary System (Oxford University Press, 2011).

- 5 - See “Capital Controls: Gates Versus Walls,” Brookings Papers on Economic Activity, Fall 2012.

SOURCE:

http://www.nybooks.com/articles/2015/12/03/new-financial-order-until-it-collapsed/